Six flagship measures to open the financial sector were promised by 1 July. They have mostly been completed. Another six will be launched by year end.

invitation to international investors

A ‘financial opening’ agenda is under way, designed to improve market access and business conditions for international investors in the financial sector. Admitting the need for international expertise to raise the performance of the financial sector, the agenda echoes China’s rationale for its 2001 WTO accession, and delivers on some still unfulfilled accession commitments. Investors have reason to be wary of empty promises, but concrete progress shows that, as domestic headlines have it, this time ‘the wolf is really here’ for inefficient domestic firms formerly protected from competition. Policy-makers have little desire to see international players challenge the dominance of domestic banks but believe that international investments will improve professionalism and remedy weaknesses in the local financial system. Incentives for investors include majority ownership of financial services companies, relaxed capital transfers to extract profits, and access to China’s thriving consumer finance market.

High-level statements have repeatedly signalled opening. The 13th financial sector 5-year plan, partially released 22 May, prioritises financial system opening and internationalisation. During Trump’s November 2017 visit, Ministry of Finance (MoF) pledged to lift restrictions on foreign investment in finance, a pledge repeated by Xi Jinping to the Boao Forum in April. Central bank governor Yi Gang 易纲 followed up with a concrete timeline, laying out six measures to be completed by end June 2018 and another six to be launched before year end. Notably, these measures aim to improve market access for foreign banks, expand business scope for foreign insurance companies, and permit foreign majority ownership in financial services joint ventures (JVs). While some of the six measures that were to be completed by end June remain out for comment in draft form, the state has taken steps to implement them all.

Policy-makers have been wary of international ideas influencing in the financial sector, especially since the 2008 financial crisis. But now, says Yi, remaining closed is more dangerous than opening. A range of factors explain this shift of perspective: domestic goals including deleveraging and moving to high-quality growth demand, modern risk management and capital allocation. A more competitive domestic sector and stronger regulators reassure policy-makers that they can open without risking foreign dominance of finance. Finally, international strategies such as the Belt and Road Initiative will require sound financing support.

mostly services sector

According to Huang Yiping 黄益平 Peking University National School of Development, financial opening has two dimensions: services and the capital account. The current opening drive, which is focused on expanding market access and business scope for foreign financial institutions, stems from Yi Gang’s 12-point plan at Boao (ten of which concern the services sector).

Beijing does not envision global investors seizing substantial market share in the domestic market; instead, for now, foreign participation is designed as a market-for-expertise trade, whereby international financial institutions are granted market share and in exchange bring best practices to the Chinese market. It hopes this will make the market stronger and more efficient. The model calls for international firms to enter niche markets directly to fill gaps in the Chinese system, while taking stakes in bigger domestic players to provide expertise. Yi has laid out what each side will bring to the table—domestic financial agencies enjoy strong business networks, whereas their foreign counterparts are better at specialised services, risk control, compliance, informatisation and product innovation. One vision is that international players directly enter niche markets to fill gaps in Chinese system, while taking stakes in bigger domestic players to provide expertise.

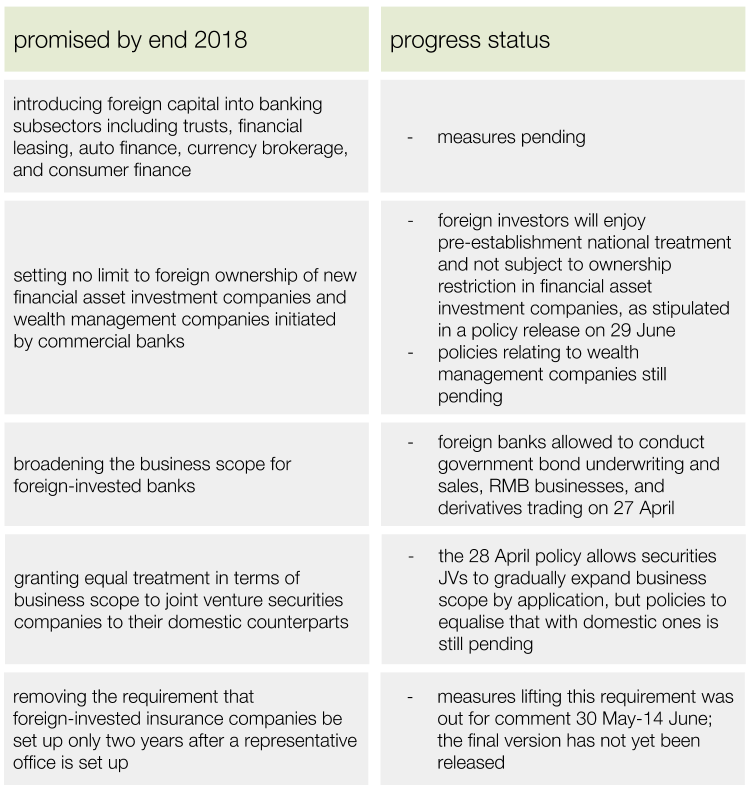

As shown below, regulators had by 1 July mostly completed the six reforms promised; one measure is still out for comment in draft form. Two of the six measures promised by end 2018 have also been completed.

Foreign investors should not assume that business expansion in China will be an easy process. Financial risk prevention is still a key focus for regulators and massive approvals of foreign investors are unlikely. But some insiders argue for a bolder opening. Instead of worrying about competing with international actors, regulators should focus on addressing difficulties encountered by foreign banks, says top government advisor Huang Yiping 黄益平, who argues

- as a highly regulated industry, ‘opening’ doesn’t mean foreign investors can come in and do anything they want; as in many other emerging markets, they may in fact find it hard to conduct business in the beginning

- networking is extremely important in the financial sector; if banks lack deep local connections, foreign investors can only get ‘a taste of the cake, not the whole cake’

- foreign investors will be subject to China’s regulatory framework

access to financial assets

Financial opening is incomplete if international players are only allowed to provide services without being able to move capital over the border and invest in China's financial assets. Recent changes have made it easier to extract profits from China. Concrete measures were released by SAFE and PBoC 12 June to make capital outflow easier for such investors. Previously, when earnings of qualified foreign institutional investors (QFII) and RMB QFII (RQFII) principals reached US$200 bn, they were subject to a three-month lockdown. After that, their monthly permitted transfer abroad is limited to 20 percent of the previous-year assets. Three major recent changes have

- cancelled overseas transfer limit of 20 percent of QFIIs total assets in the previous year

- cancelled the principal lockdown requirement for QFII and RQFII

- allowed QFII and RQFII to conduct risk hedging in the forex market

Relaxing capital outflow controls encourages inflow, benefiting capital markets; it enables foreign investors to hedge against risks, says Guan Tao 管涛 China Finance Forum 40 senior researcher, which benefits the forex market.

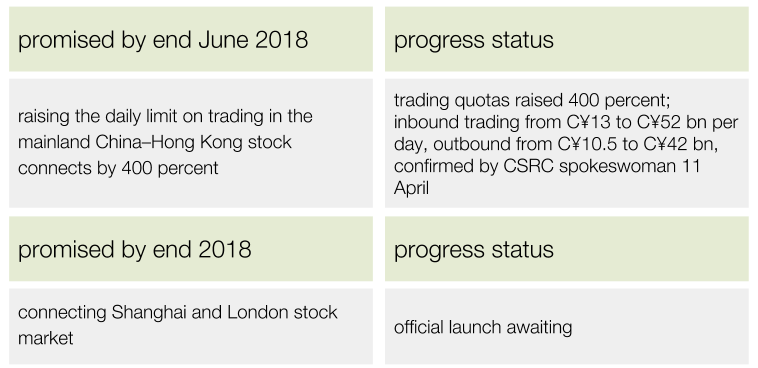

Two items on Yi’s financial opening roadmap concern fostering stock market interconnection.

Besides fostering stock market interconnection, convertibility is a key issue for capital account opening. To achieve full convertibility, the challenge becomes reducing long-term capital control while gradually relaxing short-term convertibility restriction, says Liu Cheng 刘澄 University of Science and Technology Beijing professor. Without opening, China cannot improve its external risk resilience and certainly cannot benefit from financial integration. The state should, however, have independent control over the opening process, adds Liu, ensuring that it is driven by domestic needs rather than international pressure.

At the State Administration of Foreign Exchange (SAFE) on 3 May 2018 and PBoC teleconference on 7 May 2018, Pan Gongsheng 潘功胜 People’s Bank of China (PBoC) vice governor urged steady promotion of RMB internationalisation and capital account convertibility proposing

- prioritising the use of RMB and popularising its cross-border utilisation

- advancing RMB capital account convertibility

- enhancing foundations for exchange rate marketisation

- improving macro-prudential management framework

Macro-quota management, the core element, is still in place, despite progress. The scale of QFII and RQFII is not currently significant, so opening up capital flows within the limited quota will not affect the capital market or RMB exchange rate too much, says Zhao Qingming 赵庆明 China Financial Futures Exchange chief economist. It has been noted that there are numerous obstacles to outbound investment that will not be relaxed short-term. A more optimistic outlook is that regulators are increasing the QDII quota, expanding QDLP and QDIE pilots and supporting RMB international settlement, which will foster a more balanced opening up, according to 21st Century Business Herald.

Zhou Chengjun 周诚君 PBoC Research Bureau deputy director offered two directions for future financial opening

- gradually reducing controls

- RMB-based opening

The next priority for opening will be to make RMB the driver of massive cross-border capital flows, according to Zhou.

outlook

Beijing has so far followed through on the short-term opening up promises made at Boao, and is likely to complete the medium-term list as well. With policy-makers committed to bringing in international expertise and market access, expect further opening measures to follow.

But there is still worry about invisible barriers after entry, says Cui Fan 崔凡 UIBE School of International Trade professor. Foreign players can expect limits on market share and rules that continue to protect selected national champions while importing know-how. Once more confident, Beijing has ambitions to become a decisive force in international finance. The current measures are only a first step, but, if the finance sector can deleverage and remain competitive, this ambition will drive the world into China’s markets and propel the RMB into the global economy.

timeline

15 Jun 2018: PBoC greenlights foreign commercial banks to participate in RMB spot, futures, and derivatives trading under current account and approved capital and financial accounts

15 Jun 2018: CSRC and two stock exchanges in Shanghai and Shenzhen released a series of practical regulations on CDR issuance

12 Jun 2018: revision to QFII and RQFII quota management system, facilitating cross-border capital flow

6 Jun 2018: final version of China depository receipts (CDR) and supporting policies released

30 May 2018: 234 A-shares (domestic investors only) are listed in the Morgan Stanley Capital International (MSCI) index

4 May 2018: iron ore futures market opened to international investors

4 May 2018: 'Management measures for China depository receipts (CDR)' is out for comment, one step further towards its final launch

2 May 2018: operationalising cross-border inter-bank payment system (CIPS), the so-called ‘highway’ for RMB internationalisation

20 Apr 2018: CSRC announced Lenovo to be the first pilot for H-share full mobility In addition to these flagship initiatives, financial policymakers and regulators also carried out the opening up agenda by 29 jun 2018 CBIRC 'Management measures on financial asset investment companies (provisional)' didn’t put ownership restriction for foreign investors and granted them pre-establishment national treatment

28 Jun 2018: NDRC and MofCOM released an updated foreign investment negative list granting foreign investors 51 percent shareholding in securities, securities investment fund, futures, and life insurance JVs

28 Jun 2018: CBIRC permits foreign insurance companies with over three years’ experience to participate in brokerage and surveyor businesses

8 Jun 2018: CBIRC calls for comment on a decision to repeal foreign shareholding restriction in domestic banks and asset management companies

30 May 2018: revisions to management rules on foreign insurance companies and its implementation details are under public consultation, which is expected to expand ownership cap to 51 percent, cancel requirement for setting up representative office two years before official entrance, and reduce requirements for branching activities

4 May 2018: regulation on foreign investment in futures companies undergoes public consultation

28 Apr 2018: foreign shareholding in securities joint ventures (JVs) raised from 49 to 51 percent, and the requirement that at least one of the domestic investors in a joint venture securities company be a securities company is cancelled. Securities JVs to gradually expand business scope by application

27 Apr 2018: China Banking and Insurance Regulatory Commission released a comprehensive document reiterating Yi’s proposal, which includes concrete measures like

- broadened business scope for foreign insurance brokerage firms

- expanded market access for foreign banks

11 Apr 2018: inbound (from Hong Kong to Shanghai and Shenzhen) stock trading quota enlarged to C¥52 bn per day; outbound (Shanghai and Shenzhen to Hong Kong) stock trading quota raised to 42 bn per day, confirmed by China Securities Regulatory Commission (CSRC) spokeswoman Gao Li 高莉 at press conference

who is moving the agenda?

Yi Gang 易纲 | People’s Bank of China governor

Yi was promoted to PBoC governor after serving more than ten years as vice governor in charge of monetary policy and international business. Known as level-headed, Yi cautions regulators against overreacting to market events. Not afraid to defy groupthink, Yi advocated demand-side management to avoid debt–deflation spirals during the rush to implement supply-side reform and deleveraging in early 2016. He made an even riskier departure from the Party line by calling for stabilising deleveraging in 2016, advocating limits on leverage growth rather than leverage itself. Relatively liberal on finance, Yi called for greater RMB flexibility after increased capital controls in 2015-17.

Likely picked to ensure policy continuity, Yi is expected to proceed with gradual financial market liberalisation. Topping his agenda are asset management regulation, opening the finance industry to foreign investment, and floating the RMB exchange rate. His role is limited to implementation since decision-making power remains with the Financial Development and Stability Committee chaired by vice premier Liu He 刘鹤.

People’s Bank of China (PBoC) financial stability bureau | 中国银行金融稳定局

With divisions for monitoring risks in banking, insurance, securities and financial conglomerates, the bureau is the central bank branch charged with financial stability. Mirroring the State Council’s newly set-up Financial Stability and Development Committee, it will be the latter’s new office and thus its core executive agent. It will focus on capital management in vital financial institutions, countercyclical capital management, strong interconnectivity between financial market infrastructure across industries and unified standards. Its mandate becomes more important in light of entrance of international investors increasing complexity of financial activities.

Zhu Min 朱民 | Tsinghua National Institute of Financial Research chairman

A US-trained economist, senior financial official and former IMF vice president, Zhu Min leads a research institute at the Wudaokou School of Finance, a Tsinghua–PBoC joint venture with influence on financial policy making and business practices. In a recent speech, he urges that financial regulation and opening should complement and reinforce each other. Given the fast development of fin-tech, he argues, financial regulations should progress from institutional to functional work, transcending static jurisdictions to cross regions and borders.

Guan Tao 管涛 | China Finance Forum 40 (CF40) senior researcher

Former State Administration of Foreign Exchange (SAFE) director general, Guan has participated in foreign exchange system reform since 1994. He specialises in currency convertibility, balance of payment, exchange rate policy and capital mobility. An initiator of CF40, he uses it to work with other leading minds in financial sector governance. Co-authored with PBoC economist Ma Jun 马骏, his latest book ‘Interest Rate Liberalisation and Reform of Monetary Policy Framework’ calls for a central banking overhaul, making it more professional and straightforward. There are, according to Guan, four features of the current financial opening up: regulatory neutrality, servicing the real economy, gradualism, and emphasis on supporting measures.