Hot money has cascaded down to lower-tier cities, followed by another round of purchasing restrictions, as the government balances destocking with the risk of overheating housing markets.

debt-fuelled destocking

Destocking, a focus of supply-side reform, rushed ahead in 2016. With credit cheap, buyers pounced: housing inventory fell by 3.2 percent nationally. But as prices rose, state priority shifted to curbing asset bubbles, above all in higher-tier cities, and, as mortgage growth surged, managing banking sector risks. Lending and purchasing restrictions cranked up across a swathe of tier-1 and -2 cities in October to cool markets and limit speculation. This drove hot money down to lower-tier cities.

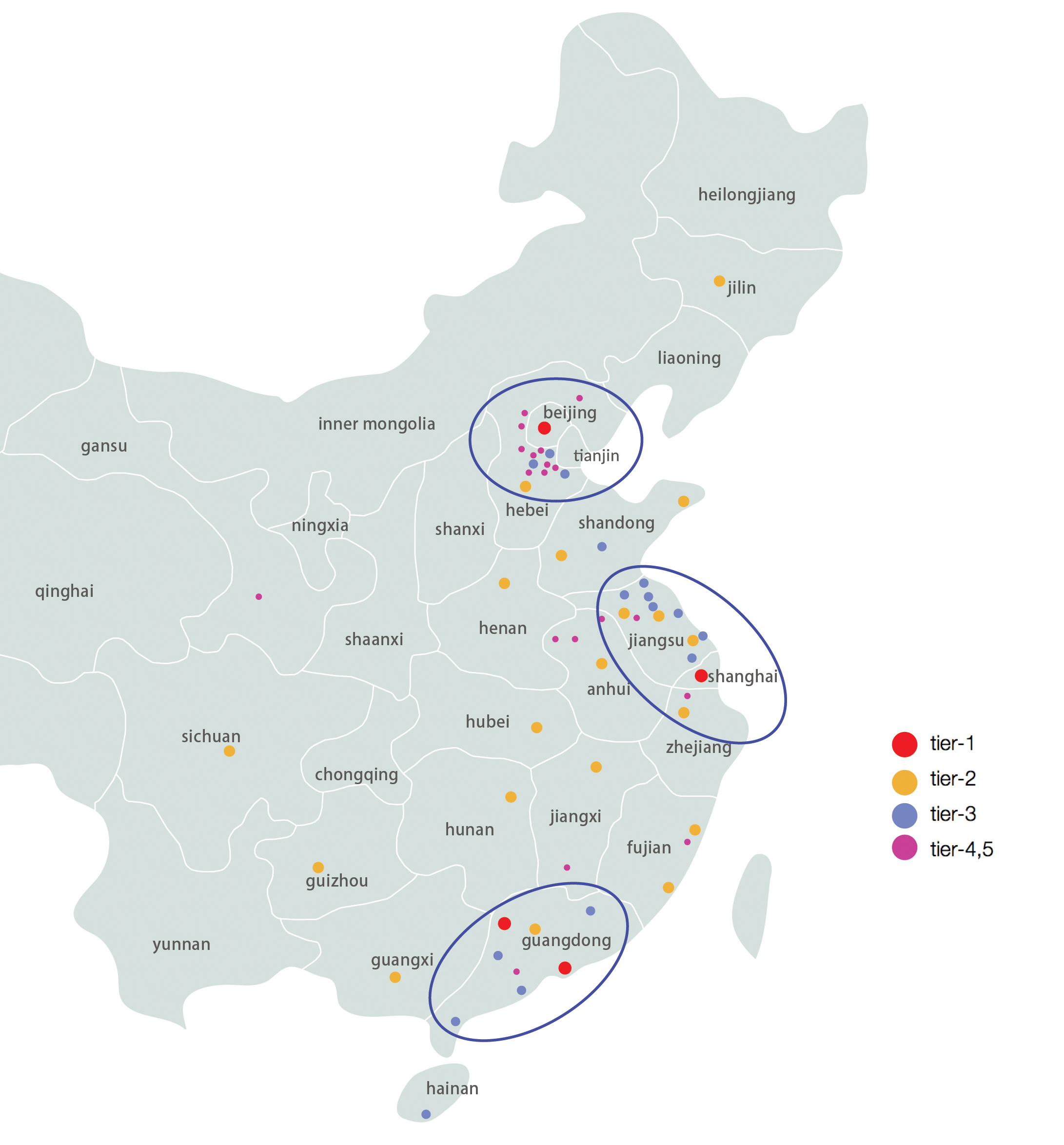

Tier-3 and -4 cities are now the main targets of destocking, according to the December 2016 Central Economic Work Conference. This was confirmed in the 2017 Government Work Report issued at the Two Sessions in March 2017, when Zhou Xiaochuan 周小川 central bank (PBoC) governor agreed credit would be directed at these tiers. This has been successful, with tier-3 cities in particular exceeding destocking targets easily. But as lower-tier markets heat up, administrative restrictions follow. New controls were launched in 70 overheating cities in March and early April, with a majority of cities facing restrictions for the first time tier-3 and below.

cities with housing purchase restrictions, March-April 2017 (blue outlines indicate urban clusters)

channelling the flood

'Housing is for living in, not speculation', said Xi Jinping 习近平 in December 2016. Yet the state encourages purchasing, and tolerates speculation, in areas of high housing inventory, only stepping in to cool things down at signs of runaway price growth. After several rounds of cuts in 2015, interest rates and the home deposit ratio are at historic lows. PBoC will adhere to a 'differentiated credit policy': making borrowing as easy as possible generally, while calling on banks to restrict lending in overheating markets through shorter mortgage periods, higher interest rates, and higher mortgage deposit ratios for additional properties. These roll out in tandem with local government purchasing controls, setting restrictions based, for example, on hukou, or on the number of years one has paid into local social security schemes.

Regulators have also moved to close market loopholes and improper behaviour. Home deposit loans from real estate agencies and P2P platforms, which reduce the threshold for and increase the leverage on property purchases, were targeted in 2016. Market manipulation, such as developers deliberately withholding finished properties to push up prices, is also in the firing line.

the great bake off

With the 19th Party Congress looming, stability is paramount. Housing is a key economic lever: government is attempting a delicate balance of sales and restrictions.

Destocking is critical to local economies. Fast growth in real estate was partly fuelled by local governments pumping up revenues through land sales, and harvesting taxes. Unsold homes represent unrealised revenue for developers too, who are keen to get idle assets off their books. Local banks, meanwhile, more risk-tolerant than PBoC, want an active real estate market, a sector still regarded as the best bet. Implicit government guarantees buoy investment, with the sector considered too important to let fail.

But demand surges pose their own set of risks. With lower-tier cities generally situated in less wealthy regions, price hikes force many aspiring homeowners out of the market, causing public dissatisfaction. With cheap credit in abundance, local banks accumulate risky levels of mortgage loans on their books. Soaring prices put downward pressure on the RMB: they push up the cost of living and labour, increasing enterprise production costs and making the export sector less competitive; investors, meanwhile, look for better returns elsewhere, adding to capital outflows.

outlook

PBoC will keep fine-tuning its differentiated credit policy to control risks. A new mortgage loan ratio policy introduced in March, for example, calls on local banks to evaluate new mortgages against total new loans in an area, to make mortgage growth reasonable.

As the market becomes more complex, however, the central bank finds it harder to encourage destocking, curb speculation, help first-time home buyers, manage those who want to upgrade, develop a better rental market, and develop social housing all at the same time. Compounding this are local governments and banks that, seeing more to gain from letting sales balloon, are reluctant to impose controls.

Supported by targeted credit and restrictions in upper-tier cities, tier-3 cities as a whole will likely continue their good January–February performance throughout 2017. Though the rising demand is artificially induced, government hopes a ‘herd mentality’ will turn this into real demand, making investment desirable even after restrictions in upper-tier cities are relaxed. But restricting buying in top-tier cities just postpones demand there, making a surge likely in 2018, after the 19th Party Congress. Tier-1 city housing, which offers double-digit annual returns, will remain the most attractive option.

context

6 Apr 2017: nine cities around Xiongan New Area impose purchase restrictions, as investors flock to buy up properties in the wake of its announcement on 1 April

3 Apr 2017: Beijing municipal government imposes purchase restrictions on single-story houses

31 Mar 2017: by end March, 50 overheated cities have collectively sold land worth C¥638 bn in Q1, up by 63.8 percent y-o-y, notes Centaline Group

30 Mar 2017: commentators criticise over-reliance on the property market for growth

29 Mar 2017: the real estate market is safe overall, with regional risks, notes Ba Shusong 巴曙松 China Banking Association chief economist; authorities should pay attention to the pressure posed by high housing prices on the banking system and RMB forex

27 Mar 2017: experts advocate long-term measures to cool down the property market

26 Mar 2017: Zhou Xiaochuan, PBoC governor, once again signals liquidity is being tightened at the Boao Forum for Asia

20 Mar 2017: Tianfeng Securities Macroeconomic Research Team notes tier-3 city housing market fragmentation, with satellite cities around the three main urban clusters—Pearl River Delta, Yangtze River Delta and Jingjinji—outperforming the rest

18 Mar 2017: National Bureau of Statistics (NBS) releases property statistics for 70 cities, noting 2 percent growth of existing home sales in 60

18 Mar 2017: PBoC releases 2017’s annual directive on bank credit and loans, stressing commercial banks must control growth of home loan portfolios and calling for pilots for real estate investment trusts

13 Mar 2017: Wei Jie 魏杰 Tsinghua University China Economy Research Centre director notes property market policy dilemmas continue

10 Mar 2017: Zhou Xiaochuan, PBoC governor, predicts home mortgage loans will continue to grow quickly, but with more attention paid to balance and prudence

9 Mar 2017: Two Sessions representatives slam developers for taking advantage of the feature town initiative

4 Mar 2017: Fu Ying 傅莹 National People’s Congress (NPC) speaker announces the government has shelved a property tax law

15 Feb 2017: nonstandard financing surged in January, following PBoC’s tightened control over banks’ on–balance-sheet lending, note commentators

20 Jan 2017: Ning Jizhe 宁吉喆 NBS director announces in 2016 real estate accounted for 6.5 percent GDP, not including construction

18 Jan 2017: National Bureau of Statistics (NBS) reports cooling down of residential housing prices in all tier-1 and and 11 tier-2 cities

12 Jan 2017: PBoC finds Chinese banks extended a record C¥12.65 tn (US$1.84 tn) in loans in 2016, 45 percent of which were for mortgages

14-16 Dec 2016: president Xi Jinping stresses housing is for living, not speculation, at the Central Economic Work Conference, where tier-3 and -4 city housing is targeted for destocking

October 2016: over a dozen cities impose purchasing restrictions during week-long National Holiday