CBRC circulated draft controls on commercial banks’ wealth management products for comment in late July 2016. More ambitious than the abandoned December 2014 proposals, they show a shift in priority from spurring growth to controlling risk.

grappling with WMPs

China Banking Regulatory Commission (CBRC) aims to control default and cross-sector risks and improve confidence in the financial system as wealth management products (WMPs) become more popular, complex and opaque. Measures would ban banks from

- offering comprehensive WMPs (which include higher risk non-standard and equity products) if they have under C¥5 bn net capital or fewer than three years of WMP experience

- issuing tiered WMPs, which slice a single investment into tranches, with some highly leveraged

- issuing equity WMPs to private investors with less than C¥1 million in financial assets or annual household income under C¥300,000 over the previous three years

They would require banks to

- engage third-party institutions to manage WMPs

- engage trust firms to issue non-standard WMPs

- maintain risk reserve funds worth one percent of outstanding WMPs to cover losses caused by bank error

with great reward comes great risk

- separating issuer from manager would control the perception of implicit guarantees by preventing banks from using their funds to cover defaults; the spurt of bank-issued WMPs largely resulted from such perceptions

- limiting high-return WMPs would reduce expectations of investment returns and signal investments should be tied to the real economy, not high-risk financial products that spawn asset bubbles

- restricting private players would limit undue risk for novice investors, while giving experienced and wealthy investors more flexibility

skyrocketing investment

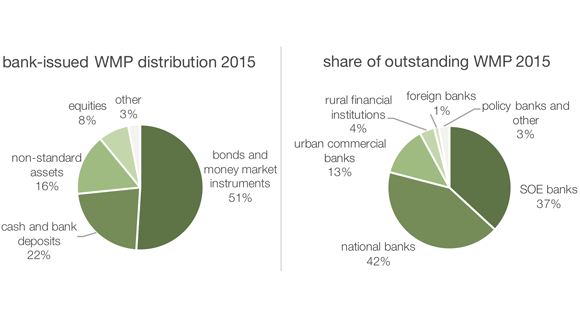

The value of bank-issued WMPs quintupled in five years, reaching C¥23.5 tn by end 2015, equivalent to a third of GDP. C¥3.8 tn or 15.7 percent of this was in non-standard WMPs and C¥1.9 tn or 7.8 percent in equity assets. Non-standard products—those not traded on the interbank market and stock exchanges—include credit loans, trust loans, acceptance bills, letters of credit and accounts receivable.

source: China Government Securities Depository Trust and Clearing Company

uncertain implementation

Previously, regulations compromising growth have often been shelved. Economic slowdown, however, increases risk of investment defaults in a ballooning sector; regulators appear resolved to push tighter controls through. Allowing banks to cross-hold each other's WMPs to meet outsourcing requirements still leaves significant room for manoeuvre. Banks may dilute restrictions further by getting

- clearance for firms other than trust firms, like securities and fund firms, to manage banks’ non-standard WMPs

- regulations to only apply to new products, tempering market disruption

- a transitional period for adjusting to the policy

A finalised policy still needs to clarify

- whether margin trading and short selling will be treated as equity asset investments

- how to handle investments containing both standard and non-standard elements

- information disclosure standards

The move likely forms part of a series of measures

- a risk management framework with indicators calculated based on net capital

- bank-issued-WMP registration and trusteeship centre to become official platform for registration and circulation

- coordinated moves by CBRC, CIRC and CSRC to reduce leverage in financial markets before the three regulators’ mooted integration

roundtable

CSRC should integrate supervision of asset management industry

Wu Xiaoling 吴晓灵 | 21st Century Business Herald

WMPs are essentially collective investment schemes, and should all be regulated by CSRC rather than three separate agencies. Banks and securities, fund, futures, trust and insurance firms all issue WMPs, but may label them differently. Fragmented supervision by CSRC, CBRC and CIRC has led to regulatory arbitrage.

banks likely to transfer risk to subsidiaries

Wei Jiyao 魏骥遥 | China Financial Times

To guard against regulatory uncertainty, banks will likely set up subsidiaries to manage riskier assets, before more comprehensive legislation on WMPs is issued. Subsidiaries will also isolate risk from banks’ core businesses as products grow increasingly complex. Falling returns pressured smaller banks to maintain growth through non-standard and equity WMPs, despite lacking qualified staff.

law on trustees needed to integrate asset management market supervision

Zhang Hongli 张红力 | Sina

NPC should formulate a law on trustees to integrate supervision over the asset management market. Funds in this industry are poised to surpass banks’ credit balances in 2016, reaching C¥120 tn. The total registered capital of funds, securities and trust firms is C¥175 bn, but they manage funds worth C¥34 tn: a leverage multiple of over 190.

context

12 Aug 2016: CSRC calls for comment on two draft policies, highlighting risk control frameworks using indicators calculated based on net capital

27 Jul 2016: draft measures to regulate commercial banks’ WMPs circulated among banks

26 Jul 2016: Politburo meeting discusses containing asset bubbles to reduce firm costs

25 Jul 2016: CBRC announces it is researching how to slow down or suspend entrusted fund management

16 Jul 2016: CSRC issues unexpectedly harsh policy on PE management by securities and future firms

16 Jun 2016: CSRC releases revised measures on controlling risk for securities firms; risk control indicators are calculated based on net capital

27 May 2016: draft measures for managing futures firms’ asset management subsidiaries released; includes risk control indicators calculated based on net capital

30 May 2016: CBRC informally requests commercial banks suspend new tiered WMPs

28 Apr 2016: CBRC reportedly releases document no. 82, banning banks from investing wealth management funds in distressed assets

18 Mar 2016: CBRC releases document no. 58, tightening supervision of trust firms

4 Jan 2016: Ministry of Finance releases enterprise accounting standard explanation no. 8, clarifying rules on controlling WMPs and their accounting. Commentators contend this prepares the ground for separating WMPs and banks

10 Dec 2014: a draft policy on bank WMP businesses was released to some institutions for comment

May 2014: CBRC moots classifying banks into three groups, each with market access to either non-standardised products, standardised products, or just consignment sales. Rejected by small- to mid-sized banks, the plan did not appear in the December 2014 draft

7 Jan 2014: State Council issues first national-level policy on shadow banking, document no. 107 ‘Circular on strengthening regulation of shadow banking’, to define it and clarify regulators’ responsibilities

25 Mar 2013: CBRC issues document no. 8, demanding assets and investment funds match, defining non-standard products, and setting up investment caps

8 Oct 2005: CBRC issues interim measures for commercial banks’ WM businesses, dividing operations into consultation, and product design and sales

in the spotlight

Li Xunlei 李迅雷 | Haitong Securities chief economist

A prolific economic commentator, Li sits on the committee for professional securities analysts. Seeing a long recession ahead for China, Li speculates the state will tighten market controls to contain the C¥120 tn property bubble and C¥15 tn bond bubble. With the financial sector’s growth—making up 9.16 percent of GDP in H1 2016—even stricter supervision is needed to control asset bubbles while reducing leverage, he says.

Hong Lei 洪磊 | Assets Management Association of China chair

CSRC Fund Department vice director for 11 years before becoming chair in October 2014, Hong is known for opening the securities fund market to private firms and individuals. WMPs should be regulated like a fund-of-funds, says Lei. Fragmented supervision of the asset management industry arises, he says, from poor legal foundations. Hong proposes revising Securities Law and Securities Investment Fund Law to regulate financial activities.

Minsheng Royal Asset Management Co, Ltd 民生加银资产管理有限公司

A subsidiary of Minsheng Royal Fund Management Co., Ltd., a joint venture of China Minsheng Bank and Royal Bank of Canada. With registered capital of C¥125 million, Minsheng Royal Asset Management oversees C¥815.6 bn, making it the second largest fund subsidiary by market share. If the draft measures are adopted, fund subsidiaries risk losing a large portion of their business to trust firms, subject to less restrictive WMP regulations.